Financial TL;DR

- $7.22B FY2024 gross fan payments (+9% YoY)

- $1.41B platform net revenue (after 80/20 creator split)

- $684M pre-tax profit (+4% YoY — slowest profit growth on record)

- 9.5% pre-tax margin on gross revenue (down slightly from 9.9% in 2023)

- Audited by external accountants — public via UK Companies House

Why these figures are uniquely auditable

OnlyFans is one of the few large creator platforms with publicly auditable financials. Its parent Fenix International Ltd is UK-registered and required to file annual accounts with Companies House. Those filings are externally audited and publicly retrievable — anyone can verify any figure on this page against the original PDF.

That's a structural advantage for analysts and journalists: most competing creator platforms (Patreon, Substack, Fansly, Fanvue) are private US/non-UK companies with no equivalent audit-disclosure obligation.

FY2024 headline figures

| Line item | FY2024 | FY2023 | YoY |

|---|---|---|---|

| Gross fan payments | $7.22B | $6.63B | +9% |

| Creator payouts (80%) | $5.80B | $5.30B | +9% |

| Platform net revenue (20%) | $1.41B | $1.31B | +8% |

| Pre-tax profit | $684M | $658M | +4% |

| Pre-tax margin (on gross) | 9.47% | 9.92% | −45bp |

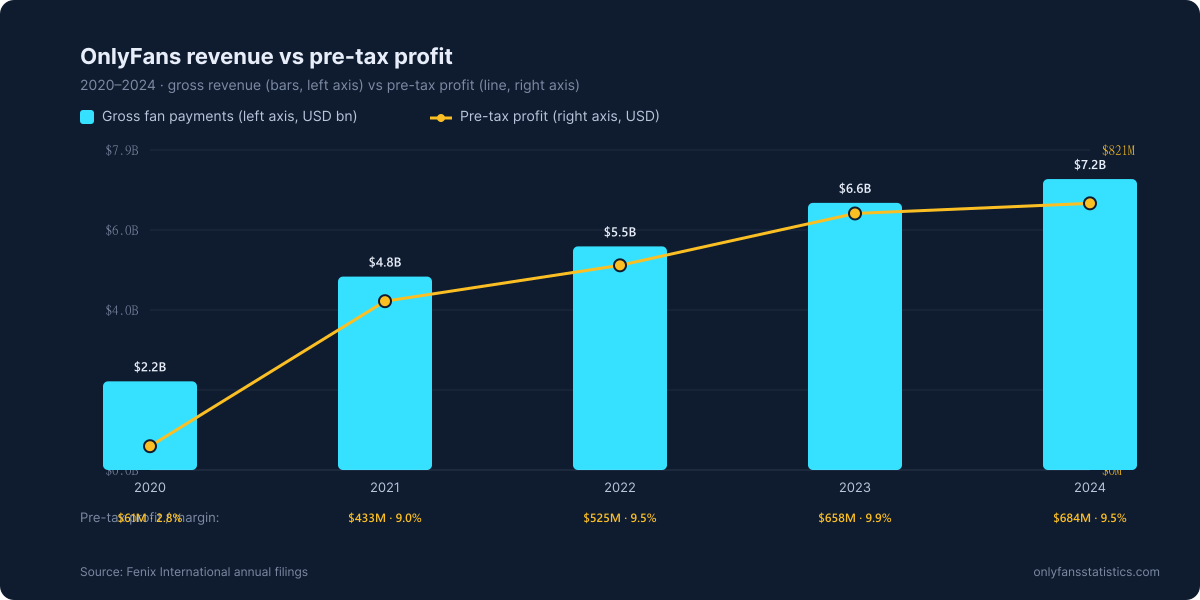

Margin compression — visualized

The single most important financial story of FY2024 is the profit-margin compression. Revenue grew 9% but profit only 4% — the first year that's happened on record.

{kind=link}

The margin trajectory: 2.8% (2020) → 9.0% (2021) → 9.5% (2022) → 9.9% (2023) → 9.5% (2024). FY2024 is the first year revenue outpaced profit growth — a signal that compliance and processing costs are eating into margins faster than revenue scaling can offset.

5-year financial trajectory

| Year | Gross | Net rev (20%) | Profit | Margin |

|---|---|---|---|---|

| 2020 | $2.20B | $0.44B | $0.061B | 2.8% |

| 2021 | $4.80B | $0.96B | $0.433B | 9.0% |

| 2022 | $5.55B | $1.11B | $0.525B | 9.5% |

| 2023 | $6.63B | $1.31B | $0.658B | 9.9% |

| 2024 | $7.22B | $1.41B | $0.684B | 9.5% |

Cost drivers behind the margin compression

Most likely contributors to the 2024 margin compression (Fenix doesn't break out individual cost lines, but external indicators support):

- Compliance infrastructure — UK Online Safety Act enforcement, EU DSA, US state-level age-verification laws all kicked in during 2024. Each requires verification, transparency reporting, and dedicated trust-and-safety headcount.

- Payment processing — adult-content category fees increased after Mastercard's 2021 rule changes. Per-transaction costs rose without proportional volume offset.

- Content moderation — 35,865 accounts removed in February 2025 alone is a significant operational expense in human review hours.

- Card-network rule compliance — Visa/Mastercard adult-platform requirements have tightened, requiring more proactive content-verification before each transaction.

Forward outlook (FY2025 expected late 2026)

The FY2025 audited filing isn't expected until late 2026. Based on traffic-side indicators (305.5M Dec 2025 monthly visits, +13% MoM growth), revenue will likely cross $7.5–8B in FY2025. The interesting question is whether profit margin holds at ~9.5% or compresses further toward 9.0%.

Sources

- [FENIX-2024] Fenix International Ltd — UK Companies House FY2024 audited filing.

- [FENIX-PRIOR] Fenix International Ltd — Prior fiscal year filings (2020–2023).

- [REUTERS-2025] Reuters — coverage of FY2024 filing release.